Scale alternatives diligence without building a larger internal team

We help capital allocators convert sponsor flow, market signals, and portfolio reporting into underwriting, monitoring, and client-ready investment views.

Pain Points for Capital Allocators

Inbound Deck Overload

Limited post-close visibility

Lack of bandwidth for pipeline development

Systematic evaluation of alternative offerings

From first-look sponsor decks to post-close monitoring, EM Capital gives allocators repeatable work product for live decisions, portfolio oversight, and stronger sponsor engagement.

More offerings, underwritten

Broader coverage without the internal headcount.

EM Capital helps allocators evaluate more sponsor flow, screen new real estate opportunities, and identify which offerings deserve deeper diligence.

Pipeline shortlist with rationale; 100% Sponsor Independent

Client Receives:

Pipeline screening

Sponsor-fit assessment

Initial diligence read

Client-fit recommendation

Faster, clearer investment views

Turn messy sponsor materials into a clear view.

Sponsor decks, PPMs, models, and reporting packages are normalized across track record, economics, fees, liquidity, reporting, and alignment.

A written assesment your team can use in the live decision.

Client receives:

Six-lens review

Normalized comparison

Key risks surfaced

Sponsor questions teed up

Independent post-close oversight

Monitor performance before the next sponsor update.

EM Capital tracks performance against underwriting, fee movement, NAV trends, leverage, thesis drift, and items to watch across allocated funds.

A quarterly read on what changed, what matters, and what to ask next.

Client receives:

Quarterly monitoring report

Performance vs. underwriting

Fund-level watchlist

Sponsor follow-up questions

More impactful discussions

Walk into the meeting with the issues already isolated.

Each deliverable identifies the highest-leverage questions and explains the risk-adjusted view, generating clear topics for IC, client updates, and sponsor meetings.

Talking points written for allocator delivery.

Client receives:

Client-ready interpretation

Sponsor questions

EM View and rationale

Next action items

Most allocators come to EM Capital at one of four moments. Choose the path that matches your live decision, send the materials, and get back decision-ready work product.

Comparing 1-4 offerings?

⬇

Start with a Decision Snapshot

Fast triage across multiple live opportunities using the six-lens framework. Receive a normalized comparison and a clear EM Capital View on each: proceed, proceed with conditions, or avoid.

Best for: first-look screening, sponsor shortlists, and

quick prioritization.

Delivery: 1-3 Business Days

Have one live deal or fund?

⬇

Start with an Underwriting Memo

Bottom-up diligence when a single decision requires conviction. EM Capital rebuilds assumptions, diagnoses fees and economics, pressure-tests downside, and surfaces the sponsor questions that matter.

Includes: allocator-ready memo, risk-adjusted view, and 60-minute executive debrief.

Delivery: 3-5 Business Days

Down to a few serious options?

⬇

Start with a Comparison Memo

Side-by-side underwriting across economics, fees, liquidity, exit path, structure, and key risks, with a relative recommendation and documented decision rationale.

Best for: final selection between multiple

credible options.

Delivery: 7-10 Business Days

Ongoing alts intelligence?

⬇

Ongoing alts intelligence?

⬇

Start with the Alternative Intelligence Suite

Ongoing alternatives research: biweekly meetings, quarterly monitoring, ad-hoc underwriting/comparisons, RE pipeline development, and Resi-Alpha access, powered by Steuart AI.

Best for: ongoing monitoring, pipeline development, and

team leverage.

Implementation: 4 Weeks

Ad Hoc vs. Suite

Ad Hoc is fixed-scope work for a specific decision. You send one live deal or set of offerings; we deliver a memo within 1 to 10 business days. Best when decisions are episodic.

The Suite is an ongoing engagement, we become your alternatives research function. Best when you have a steady flow of decisions and want monitoring, pipeline, and underwriting under one roof.

How Long Does It Take?

Ad Hoc deliverables turn around in 1 to 10 business days, depending on materials and complexity.

The Suite onboarding takes about four weeks, portfolio mapping, data intake, monitoring framework setup, and pipeline configuration, before settling into a biweekly rhythm.

Pricing and turnaround are confirmed in the engagement letter.

Send One Live Decision

The fastest way to see how we work is to send us something real. One deal, one fund, one comparison, and we'll get back to you with a decision-ready work product.

Elite Broker Blogs

━━━━━━━━

AI should scale judgment, not administration

AI should scale judgment, not administration

How a question about buying rentals became a market-intelligence system for allocators.

By Daniel Erb

Most firms are using AI to move faster through work that was never the source of investment edge: summarizing a deck, drafting an email, populating a CRM, or automating a recurring deliverable. Those uses are practical. They are also low leverage.

The harder question is whether AI can expand and improve the research process behind capital allocation: test more hypotheses, compare more markets, and identify where a compelling story may not be a compelling use of capital.

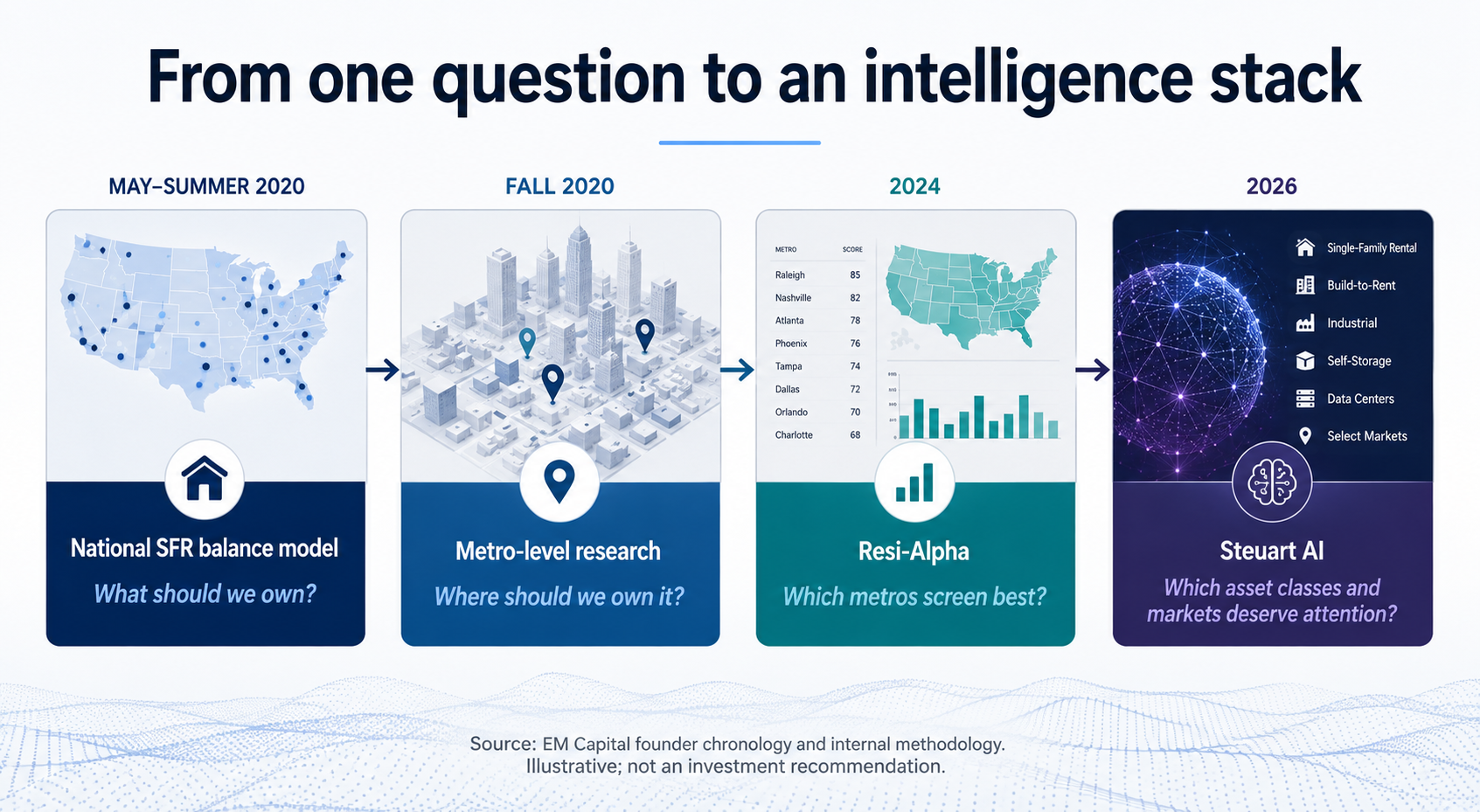

Steuart AI began as our attempt to answer that question for ourselves. It did not start as software. It started in May 2020 with a decision about where to invest our own money.

The highest-value use of AI in alternatives is not automating administration. It is scaling the research discipline that determines what deserves allocator attention.

That distinction matters. Alternatives are not short of information. They are short of independent, comparable judgment.

Every sponsor can explain why its asset class, market, manager, and timing are attractive. An allocator still has to determine which parts of that argument are structural, which are cyclical, which are already reflected in price, and which deserve deeper underwriting.

Steuart is designed to increase the number of those questions we can test. It is not a chatbot, a summary tool, or a recommendation engine. It is EM Capital Management’s broader intelligence environment, built from the buyer’s side: a proprietary research stack that applies the supply-and-demand logic, demographic analysis, validation process, and human governance we first developed for single-family rentals across a wider real estate opportunity set.

The objective is not to replace investment judgment. It is to give judgment a larger, better-tested evidence base that learns and improves 24/7.

This is the first time we have discussed Steuart publicly. Until now, it has been available only in limited use to clients of EM Capital’s Alternative Intelligence Suite. From one question to an intelligence stack

1. We started with the dollar, not the backyard

In May 2020, William McSweeney, CFA and I decided to partner on a real estate investment. We both worked in finance, had dry powder, and viewed real estate as a way to build long-term wealth tax-efficiently.

But we did not begin the way many emerging real estate operators begin: with what we could afford, what was geographically convenient, or what we already knew how to operate.

We began with a research question:

What was the best use of the next dollar?

Single-family rental stood out for three reasons. Demand was growing. Ownership was fragmented enough for disciplined buyers to find pricing advantages. And housing supply did not adjust evenly to household demand.

William adapted a commodity-style balance framework he had used while covering oil and gas at BlackRock, where forward supply-and-demand estimates informed investment decisions measured in billions of dollars. At a national level, the model asked a basic question: how much demand was forming, how much supply was coming, and what did the resulting gap imply?

By the fall of 2020, we had pushed the work to the metro level. We tested demographic and economic variables including median income, median age, home prices, population growth, and income growth. The process was manual, which limited the number of markets and hypotheses we could test.

But the principle was established: build the thesis, test it, and let the evidence narrow the map before committing capital.

That discipline later informed millions of dollars of rental-property acquisitions through EM Capital Management partner funds, joint ventures, and Strand Capital LLC .

The name Steuart came later, as a reference to Sir James Steuart’s supply-and-demand thinking. The operating logic was there from the beginning.

2. Resi-Alpha made the process repeatable

The philosophy became operational in 2024, when we built the data pipelines, data lake, cleaning processes, and automated pulls required to move beyond one-off analysis.

That system became Resi-Alpha, which remains Steuart’s residential scoring engine.

Resi-Alpha now screens 386 U.S. metros using more than 300 inputs, updated monthly. It assesses growth potential, overheating, bubble risk, and market stress. Its live capabilities include:

Comparing metros on a common basis

Producing three-year home-price growth with strong historical backtest performance

Separating rent growth from potential cap-rate compression

Identifying similarly sized markets with stronger scores

Detecting overheating and bubble risk

Producing automated market reports

The point is not that a model can eliminate uncertainty. The point is that a repeatable process increases hit rates and can be tested.

Across 13 annual vintages beginning in 2010, Resi-Alpha’s top-30 metro selections beat the median metro by an average of 8.9 percentage points over the following three years, 26.8% cumulative growth versus 17.9%. The selections outperformed the median in 12 of 13 vintages and identified eventual top-decile metros at approximately 3.7 times the rate implied by random selection.

Those are hypothetical, backtested results, not client returns. They do not prove that any future market call will be right. They do show that market selection can be treated as a disciplined, falsifiable research problem rather than a collection of anecdotes.

The visual on page 12 of EM Capital’s May 2026 Capabilities Overview summarizes the operating design: more than 300 inputs feed a scoring engine built around pattern recognition, sensitivity analysis, composite scoring, and human governance. The governing principle is explicit: underwriting decides; the model informs.

3. Steuart expanded the question from “where” to “what”

At the beginning of 2026, we began building Steuart as the broader intelligence environment around Resi-Alpha.

The first expansion returned us to the question we asked in 2020: before deciding where to invest, which asset class deserves the dollar?

Today, Steuart produces a live national ranking across nine real estate categories:

Single-family rental, multifamily, office, industrial and logistics, self-storage, retail, senior housing, manufactured housing, and data centers.

The system compares a category’s expected return with the risk-adjusted hurdle it must clear. Supply, demand, liquidity, market structure, and the price paid for growth provide context for what may drive the result. Steuart then translates that work into relative positioning, overweight, accumulate, hold or trim, and underweight, as a screening view, not an investment directive.

That distinction is useful because a real estate mandate should not begin with the asset class that's most convenient, but with the best opportunity set. It should begin with the opportunity set.

A client asking for “real estate exposure” may be better served by a different category, market, or entry point than the first sponsor presentation suggests. Steuart gives an advisor a basis for explaining what is available, what economic forces are reshaping the categories, and why one use of capital may be preferable to another.

For single-family rental, Steuart can already move from the national view to detailed metro comparisons and automated report production. Multifamily metro analysis and its bubble detector are in client beta. The cross-asset national ranking and automated reporting are live.

The Q2 2026 Cross-Asset Real Estate report demonstrates the current national application across all nine categories while also stating where the model’s sample size and data coverage limit precision.

4. The limit is the point

Steuart is currently a powerful idea generation tool, not a recommendation engine.

Real estate is location-specific, function-specific, manager-specific, and structure-specific. A national category score cannot determine whether a particular asset, fund, or joint venture should be purchased. Basis, leverage, fees, liquidity, sponsor execution, reporting, asset quality, and deal structure still require separate underwriting.

That boundary is deliberate.

Steuart can indicate that a category or market deserves more attention, that a thesis appears fully priced, or that a comparable market has a more favorable setup. It cannot say, on that evidence alone, “buy this fund.”

We are building depth before claiming certainty, and we are not done expanding or improving our capabilities. The Q3 2026 build priorities are:

Complete multifamily metro-level coverage. Bring multifamily market selection to the standard already applied in single-family rental.

Expand bubble and stress detection. Improve the system’s ability to distinguish durable growth from conditions that depend on unsustainable price, supply, financing, or migration assumptions.

Separate broad categories into investable subcategories. Build out healthcare as a distinct real estate class and distinguish logistics-oriented industrial from manufacturing assets rather than treating every property under one industrial label as economically interchangeable.

Steuart is built vertically. EM Capital Management owns the code and intellectual property, maintains and guides the proprietary research curriculum, and runs agentic workflows that can test hypotheses and propose methodological changes without waiting for an analyst to formulate every individual prompt.

Human review still approves changes to the methodology. The system can propose. It cannot approve its own research standards. Client and sponsor data are not used to train a shared external model.

THE FRAMEWORK

The Four-Decision Stack

Every private real estate decision can be separated into four layers:

1. Class

What exposure should the dollar own?

This is the national allocation question: single-family, multifamily, industrial, retail, data centers, or another category.

2. Market

Where should that exposure be deployed?

Real estate can have wide regional performance dispersion. So the geographic question becomes: which metros have the most favorable combination of demand, supply, affordability, price, growth, and stress?

3. Operator

Who can execute, and what function does the asset serve?

Two properties carrying the same broad label may have entirely different operating requirements and demand drivers. A logistics facility is not a manufacturing plant. A trophy office asset is not a commodity downtown tower. The manager’s capabilities have to match the asset’s actual function.

4. Terms

At what basis, leverage, fee load, liquidity, and governance?

A sound asset class, market, and operator can still become a poor investment when the entry price, capital structure, fees, or investor protections are wrong.

Most sponsor materials begin at Layer 3. The operator presents the strategy, asset, and track record, then explains why the market supports the deal. Many allocator processes begin there too, because that is where an available product enters the pipeline.

The better order is the reverse.

First determine whether the asset class deserves attention. Then identify the markets where the fundamentals are strongest or the risks are mispriced. Only then compare operators and terms.

Steuart is currently strongest in the first two layers. EM Capital’s underwriting process addresses the last two. The Alternative Intelligence Suite connects them: market intelligence can shape the mandate, challenge a sponsor’s assumptions, and then be incorporated into a sponsor-specific underwriting memo.

This is also the correct way to judge any AI system marketed to investors. Ask which layer it improves.

An application that summarizes the sponsor’s materials may make Layer 3 faster. A system that tests the opportunity set before the sponsor enters the room may improve the allocation decision itself.

WHAT THIS MEANS FOR ALLOCATORS

Access to Steuart does not mean a software login or an ungoverned conversational interface.

It means access to a standing research function.

Alternative Intelligence Suite clients can request unlimited Resi-Alpha and cross-asset reports on demand rather than waiting only for a quarterly publication. They receive the quarterly cross-asset view, review the work during biweekly meetings, and can incorporate sponsor-specific market outputs into underwriting memos.

In its limited client use to date, that work has helped a client pause an investment, helped an advisor explain alternatives to an end client in plain English, and redirected a mandate toward a different asset class or market.

Those are not claims that Steuart made the final decision. They are examples of what better screening changes: the advisor enters the conversation with an independent view, the sponsor faces better questions, and the allocator spends diligence time on the opportunities most likely to earn it.

The practical gain is not more content. It is a better order of operations:

Universe first. Market second. Sponsor third. Terms fourth.

That gives advisors a documented evidence base for discussing alternatives with the same discipline they apply to public markets, without pretending that a model can replace manager selection, asset underwriting, or investment judgment.

Access tells an allocator what is available. Intelligence tells them what deserves attention.

Request a sample Steuart report to review the full methodology, current output, and stated limitations.

SOURCES & METHODOLOGY

EM Capital founder chronology, May 2020–June 2026. Founding history and development timeline provided by Daniel Erb, including William McSweeney’s role in adapting the commodity-style balance framework.

EM Capital Management, Capabilities Overview, May 2026. Resi-Alpha’s 386-metro coverage, representative 300-plus inputs, monthly update cadence, analyst governance, model limitations, and Alternative Intelligence Suite operating cadence. See especially pages 12, 16, and 24.

EM Capital, Cross-Asset Real Estate Quarterly Report, Q2 2026. Nine-category framework, approved Resi-Alpha backtest, cross-asset methodology, forward-looking model limitations, and disclosures. See especially pages 1–3 and 25–26.

EM Capital, Introducing Steuart AI, June 2026. Buyer-side platform definition, independent-view positioning, and distinction from chatbots and summary tools.

Methodology note: Resi-Alpha backtest figures are hypothetical and backtested, not actual client or trading results. Past or backtested results do not guarantee future performance. Market-level signals do not predict fund-level returns; asset quality, basis, leverage, manager execution, fees, liquidity, and structure remain separately underwritten.

Daniel Erb is co-founder of EM Capital Management and leads execution and strategy across real estate investing and allocator-side decision support.

For discussion purposes only. Not an offer to sell or solicitation of securities. Not legal, tax, regulatory, or investment advice. EM Capital Management does not act as a placement agent. Model-generated and forward-looking figures depend on assumptions and may differ materially from actual outcomes.