Solving the capacity gap between

sponsor flow and allocator

underwriting

As Featured In

━━━━━━━━

Alternative Investment Intelligence for the Decision in Front of You

EM Capital helps allocators turn sponsor decks, models, reporting packages, and market data into decision-ready work product, from fast triage to full underwriting, monitoring, and pipeline development.

When Comparing 1-4 Offerings

Receive a normalized comparison to determine whether to proceed, diligence further, or avoid.

When an offering requires further conviction

Rebuilt assumptions, fee and economics diagnosis, downside sensitivity, leverage and liquidity review, and a risk-adjusted view.

2-3 serious options under active consideration

Side-by-side underwriting, with economics, fee structure, liquidity, exit path, key risks, and decision rationale clearly documented.

For ongoing alternatives research support

A permanent intelligence layer across the alternatives sleeve, powered by Steuart AI: biweekly working meetings, quarterly monitoring reports, on-demand underwriting and comparison support, active real estate pipeline development, and Resi-Alpha analytics access

Underwriting, acquisitions, portfolio analytics, real estate research, and investor-facing experience.

Daniel Erb

Execution & Strategy

William McSweeney, CFA

Market & Portfolio Analytics

Laetizia Bizzari

Underwriting & Economics

HOW TO ENGAGE

Start with decision in front of you

Most allocators come to EM Capital at one of four moments. Choose the path that matches your live decision, send the materials, and get back decision-ready work product.

Comparing 1-4 offerings?

⬇

Start with a Decision Snapshot

Delivery: 1-3 Business Days

Have one live deal or fund?

⬇

Start with an Underwriting Memo

Delivery: 3-5 Business Days

Down to a few serious options?

⬇

Start with a Comparison Memo

Start with an Comparison Memo

Delivery: 7-10 Business Days

Need ongoing alt intelligence?

⬇

Start with the Alternative Intelligence Suite

Implementation: 4 Weeks

TURN SIGNALS INTO ACTION

Subscribe to our newsletters

FEATURED

The Private Credit Diligence Gap

TAM · Edition 8 · May 2026

The Allocation Memo

Built for the allocator's desk

Dan's weekly read on capital flows, allocation strategy, and the residential alpha thesis. For RIAs and Family Offices.

Weekly

Against The Tape

Stress-testing the consensus

Our standing exercise in arguing the other side of market consensus, not because we believe it, but because we don't trust a thesis we haven't stress-tested.

Bi-weekly

Select Features

━━━━━━━━

Send One Live Decision

The fastest way to see how we work is to send us something real. One deal, one fund, one comparison, and we'll get back to you with a decision-ready work product.

Jamie Dimon Saw A Cockroach

Jamie Dimon Saw A Cockroach

The Pension Funds Just Raised Their Targets

J.P. Morgan's CEO has been warning about private credit for over a year. The market just crossed $3.5 trillion. His own annual letter says it's not systemic.

Your client just forwarded you a Bloomberg headline about Jamie Dimon's latest warning on private credit. He's seen the "cockroach" quote. He wants to know if his allocation is safe. He's using the word bubble.

Here's the good news. He's not wrong that there's stress in the market. He's wrong about what Dimon actually said, and he's wrong about what the stress means.

This piece is for that conversation.

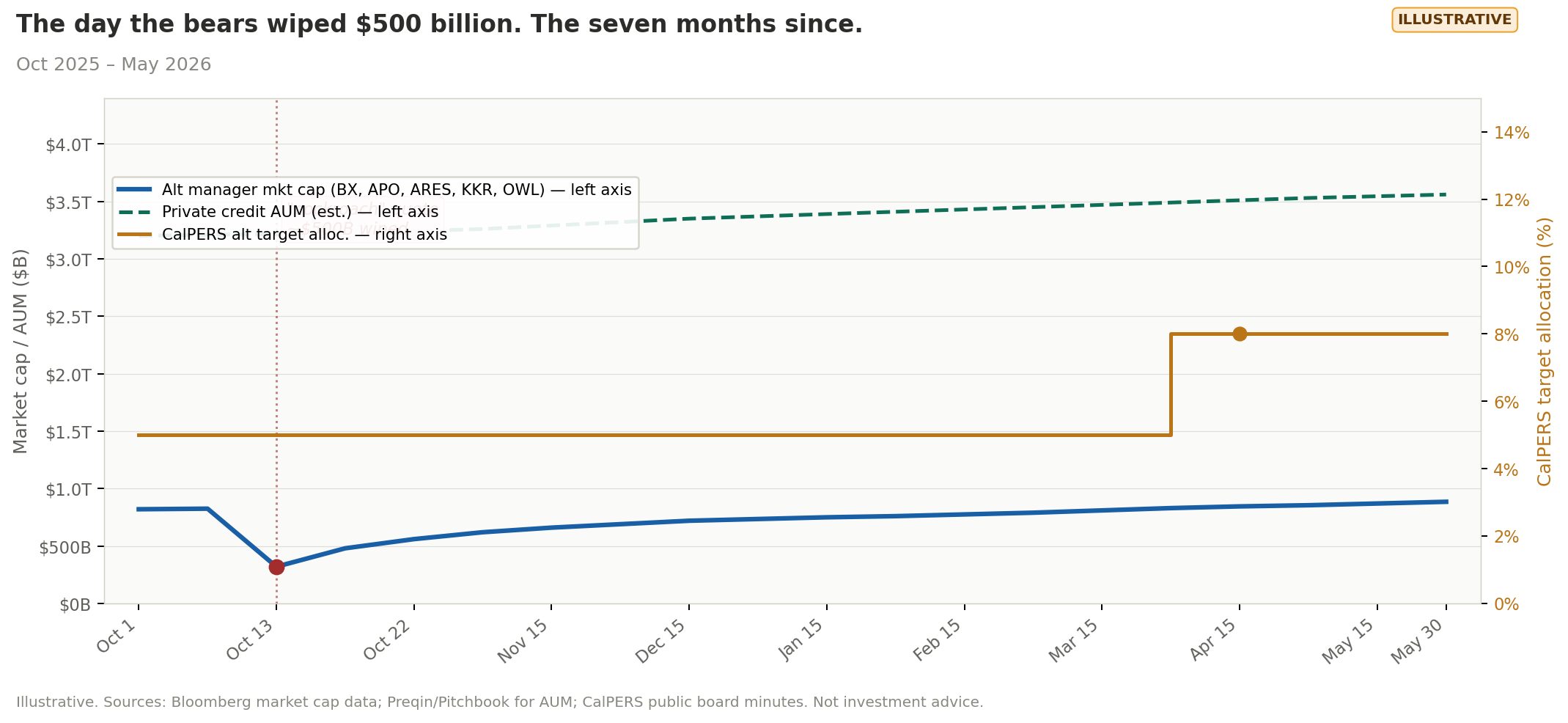

The Day The Bears Wiped $500 Billion. The Seven Months Since.

Against The Tape is our standing exercise in arguing the other side of market consensus, not because we believe it, but because we don't trust a thesis we haven't stress-tested. Built for advisors, allocators, and anyone whose job is to have a real answer when consensus gets loud. Published every 2 to 4 weeks. Not our base case. Not investment advice.

Private credit is a $3.5 trillion accident waiting to happen. Overleveraged, opaque, untested in a real downturn, held together by amend-and-extend duct tape. Jamie Dimon has been ringing the bell for over a year. The defaults are rising, the redemptions are piling up, and it's only a matter of time before the whole thing comes undone. That's the room. Here's the strongest case the room is wrong.

The bear case has teeth, and the headlines have been writing themselves. In October 2025, Dimon told JPMorgan analysts, "When you see one cockroach, there are probably more, and so everyone should be forewarned of this one." That single line is reported to have erased roughly $500 billion in value from alternative asset managers in a single day. At the Norges Bank conference in April, he warned that "when there's a credit cycle, losses will be worse than people think." The Financial Stability Board flagged structural risks in May. Fitch put the trailing 12-month default rate at 5.8% in January, the highest in the asset class's history. A major retail fund froze redemptions after $5.4 billion in withdrawals hit at once. Another shop had to inject $400 million of its own capital to satisfy a separate redemption queue. First Brands went bankrupt after lenders discovered they'd underwritten a company at 5x leverage that was actually running 20x, with the extra leverage hidden off the balance sheet. Tricolor went into Chapter 7 after employees were pledging the same loans multiple times and fabricating VIN numbers. UBS modeled a worst-case AI disruption scenario for software borrowers, who make up a quarter to a third of private credit portfolios, and got a 13% default rate.

If you squint at it a certain way, it looks like a lot of smoke.

And then there's what Dimon actually said in his shareholder letter.

In his April 2026 annual letter, Dimon wrote that "in the great scheme of things, private credit probably does not present a systemic risk." On JPMorgan's next earnings call he went further. "It almost can't be systemic at that size relative to anything else. I'm not particularly worried about it." The loudest bear in the market gave the bulls their punchline. The financial press kept the cockroach.

While Dimon's nuance was getting flattened into a one-line headline, the world's most conservative institutional capital was moving the other way. CalPERS raised its private credit target from 5% to 8%. Global public pension funds went from 2.9% allocation in 2020 to 4% in 2024, and they're still climbing. LP inflows hit $300 billion in 2025. The largest manager in the space crossed $1 trillion in AUM this month. The market that was supposed to be melting down is growing faster than the headlines saying it can't.

The bears didn't ignore the stress. They priced the wrong story onto it.

Three reasons the other side has a case:

Private credit defaults look higher than public credit defaults because the covenant structure surfaces problems earlier, not because the underwriting is worse.

Private credit funds run 35% debt to 65% equity. The entities running 90%+ leverage in this ecosystem are the banks, not the funds.

The world's most conservative institutional capital is moving in, not out. Pension funds are at a four-year high. Even Dimon himself says it's not systemic. The scoreboard and the forecast don't agree.

The default rate is measuring the wrong thing. Direct lending agreements carry maintenance covenants, financial ratios borrowers must hit quarterly, that trigger lender engagement before a company blows up. High-yield bonds are covenant-lite. Problems in public credit markets stay hidden for months, sometimes years, until the filing hits and there's nothing left to recover. The higher disclosure rate in private credit isn't worse underwriting. It's better early warning. Fitch's 5.8% figure and Proskauer's 2.71% figure aren't contradictions. They're measuring different things. One counts formal defaults, the other counts covenant breaches resolved before the company fails. A market that surfaces problems early and resolves them quietly is not a bubble about to pop. It's credit working as designed.

The leverage is in the wrong place for a bubble. The classic bubble playbook requires leverage applied to assets whose prices have disconnected from fundamentals. Private credit funds run approximately 35% debt to 65% equity. That's conservative by almost any standard. The institutions writing the bubble warnings run north of 90% leverage. The entities in this ecosystem actually running hot are the banks with $220 billion in direct exposure to private credit. The Fed's June 2025 stress tests confirmed banks stay above minimum capital requirements under private credit shock scenarios. The Financial Stability Board's own report, the same one generating the scary headlines, states explicitly that private credit is not systemically risky at current scope. Dimon, in his own letter, said the same thing. The First Brands and Tricolor collapses were fraud, not structural failure. The leverage risk is real. It's just not where the bear thesis says it is.

The smart money is moving in the opposite direction from the narrative. CalPERS raised its target from 5% to 8%. Global pension funds went from 2.9% in 2020 to 4% in 2024 and are still climbing. 86% of global institutional investors expect to be allocated to private debt within three years. Private credit now funds 90% of middle-market buyout financing, up from 36% in 2014. These are not momentum chasers. These are fiduciaries with investment committees and legal obligations to their beneficiaries. They've read the FSB report. They've read Dimon's letter. They've seen the cockroach headlines. They're still raising allocations. When the world's most conservative institutional capital diverges from the financial media on an asset class, one of them is doing the work and one of them is writing clicks.

Add it up. The default signal is methodological, the leverage lives in the banks, and the capital doing serious underwriting is moving the other way. The stress is real. The bubble is a story about the stress.

The Talking Points. Three lines for the client call:

"The cockroach quote made a great headline. But Dimon's own annual letter, the one nobody read past page three, says private credit 'probably does not present a systemic risk.' That's the loudest bear in the market telling you not to call this a bubble."

"Private credit funds run 35% debt to 65% equity. If you want to find the dangerous leverage in this ecosystem, look at the banks with $220 billion of direct exposure, not the funds they're lending to."

"CalPERS raised their target from 5% to 8%. Global pensions are at a four-year high in private credit allocation. When the world's most conservative institutional capital is moving into something while the financial press calls it a bubble, that's worth a second look."

The Themes. If the contrarian read is right, where does it point?

The crowded trade is the easy one to spot. Redemption-freeze stories and meltdown narratives have spooked retail capital out of the asset class entirely. Avoidance has become the consensus position, built on conflating idiosyncratic fraud cases with structural market failure. By the time a thesis is on every front page, the easy edge is gone.

The interesting trades are the ones the panic obscured. Senior secured direct lending is yielding meaningfully above comparable public instruments right now, and the spread is being left on the table by capital that took the headlines at face value. The dispersion inside the asset class is the real story. Funds that chased yield by loosening covenants are the ones in the headlines. Funds running disciplined credit processes with real workout infrastructure are not the same product, and the market is pricing them as if they were.

The trade nobody's talking about is structural, not tactical. Every cycle where private credit absorbs a real stress event and keeps growing makes the next bubble call less credible. That's not a position, that's a regime. The asset class is being institutionalized in real time. The longer the scoreboard and the forecast disagree, the more capital flows toward the discipline that compounds in this market. Manager selection. Workout infrastructure. The boring stuff that doesn't make for good cable news.

Jamie Dimon saw a cockroach. The pension funds raised their targets. The bears have called private credit a bubble at every trillion, and the market is over $3.5 trillion. Even Dimon's own letter says it's not systemic. At some point, the forecast has to explain the scoreboard.

Against The Tape is published every 2 weeks. An exercise in arguing the other side, not our base case. Not investment advice.