Solving the capacity gap between

sponsor flow and allocator

underwriting

As Featured In

━━━━━━━━

Alternative Investment Intelligence for the Decision in Front of You

EM Capital helps allocators turn sponsor decks, models, reporting packages, and market data into decision-ready work product, from fast triage to full underwriting, monitoring, and pipeline development.

When Comparing 1-4 Offerings

Receive a normalized comparison to determine whether to proceed, diligence further, or avoid.

When an offering requires further conviction

Rebuilt assumptions, fee and economics diagnosis, downside sensitivity, leverage and liquidity review, and a risk-adjusted view.

2-3 serious options under active consideration

Side-by-side underwriting, with economics, fee structure, liquidity, exit path, key risks, and decision rationale clearly documented.

For ongoing alternatives research support

A permanent intelligence layer across the alternatives sleeve, powered by Steuart AI: biweekly working meetings, quarterly monitoring reports, on-demand underwriting and comparison support, active real estate pipeline development, and Resi-Alpha analytics access

Underwriting, acquisitions, portfolio analytics, real estate research, and investor-facing experience.

Daniel Erb

Execution & Strategy

William McSweeney, CFA

Market & Portfolio Analytics

Laetizia Bizzari

Underwriting & Economics

HOW TO ENGAGE

Start with decision in front of you

Most allocators come to EM Capital at one of four moments. Choose the path that matches your live decision, send the materials, and get back decision-ready work product.

Comparing 1-4 offerings?

⬇

Start with a Decision Snapshot

Delivery: 1-3 Business Days

Have one live deal or fund?

⬇

Start with an Underwriting Memo

Delivery: 3-5 Business Days

Down to a few serious options?

⬇

Start with a Comparison Memo

Start with an Comparison Memo

Delivery: 7-10 Business Days

Need ongoing alt intelligence?

⬇

Start with the Alternative Intelligence Suite

Implementation: 4 Weeks

TURN SIGNALS INTO ACTION

Subscribe to our newsletters

FEATURED

The Private Credit Diligence Gap

TAM · Edition 8 · May 2026

The Allocation Memo

Built for the allocator's desk

Dan's weekly read on capital flows, allocation strategy, and the residential alpha thesis. For RIAs and Family Offices.

Weekly

Against The Tape

Stress-testing the consensus

Our standing exercise in arguing the other side of market consensus, not because we believe it, but because we don't trust a thesis we haven't stress-tested.

Bi-weekly

Select Features

━━━━━━━━

Send One Live Decision

The fastest way to see how we work is to send us something real. One deal, one fund, one comparison, and we'll get back to you with a decision-ready work product.

AI Will Split Private Markets in Two

AI Will Split Private Markets in Two

Scale wins. Focus wins. The vague middle gets squeezed.

Most conversations about AI in private markets are too narrow. They start with tools. Which model will analysts use? Which data platform wins? How many hours can be saved in diligence? Those questions matter, but they miss the bigger opportunity.

The real market is not AI software spend. The real market is the decision layer around private capital itself.

Alternative AUM was $16.7 trillion in 2024 and is projected at $30.0 trillion by 2030, according to EM Capital's capabilities deck, which cites Preqin, IMF Global, and OECD. The same deck frames the allocator problem plainly: alternative allocation is growing faster than decision infrastructure. It points to more sponsor decks than any team can underwrite, limited time to rebuild diligence, and blind spots between sponsor updates.

This is the TAM for AI in private markets: not replacing investors, but rebuilding the infrastructure that helps allocators and managers decide what deserves capital, attention, and monitoring burden.

AI will not make private markets easy. It will make weak process easier to expose.

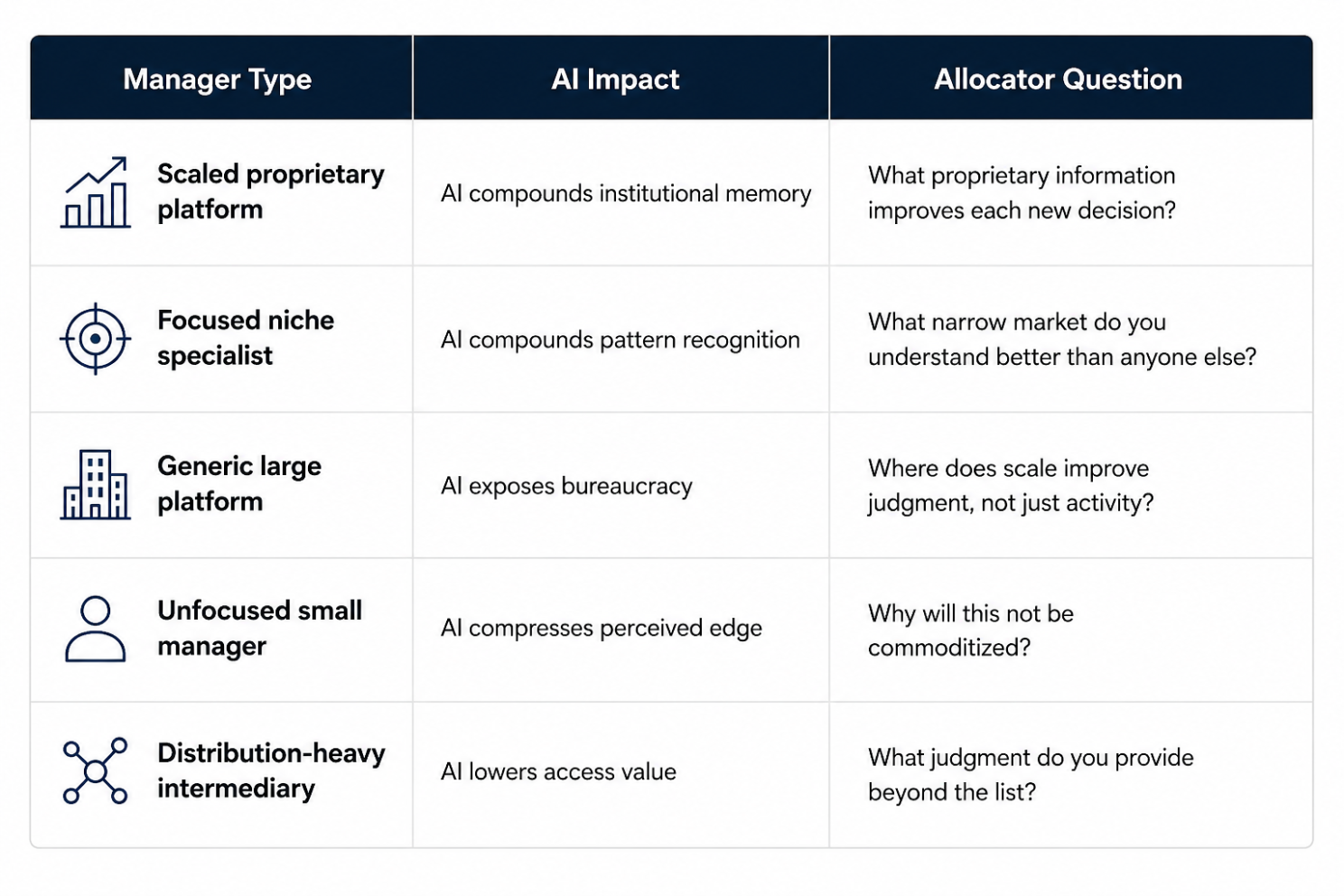

For allocators, the question is no longer whether a manager has access, a polished deck, or a familiar story. The question is whether that manager has an edge AI will compound, or an edge AI will commoditize.

The next advantage in private markets will come from two places: scale and extreme focus. Everyone else will need better architecture.

Scale matters because large firms sit on proprietary data: prior deals, failed deals, investment committee memos, operating histories, customer references, portfolio company reporting, expert notes, and years of institutional judgment. AI makes that memory usable.

Extreme focus matters because niche specialists can build pattern recognition that a generalist cannot fake. A manager who has spent a decade in one narrow market has a different type of data asset. It may not be large in absolute terms, but it is dense.

The middle is the problem.

The unfocused manager, the generic advisor, the data-only platform, and the broad consultant with thin conviction all face the same pressure. AI lowers the cost of first-pass research. It raises the value of proprietary judgment.

1. Scale turns institutional memory into an operating asset

The best large firms are not advantaged because they have more junior analysts.

They are advantaged if they can turn proprietary memory into a live underwriting system.

A scaled private markets platform has seen hundreds or thousands of deals. It has passed on more than it has closed. It has watched sponsor projections age into actual operating results. It has seen which customer references were predictive and which were noise. It has built value creation plans that worked and others that failed inside the first 90 days.

Historically, much of that knowledge was trapped.

It sat in old memos, shared drives, diligence folders, board decks, meeting notes, partner recollections, and portfolio reporting packages. The knowledge existed, but it was hard to retrieve at the point of decision.

AI changes that.

A scaled firm can now ask better internal questions:

What did we learn the last five times we reviewed this business model?

Where did management teams tend to overstate margin expansion?

What warning signs appeared before performance broke?

Which assumptions failed because of capital structure, not operations?

Which customer calls changed the investment view?

That is not just productivity. That is institutional memory becoming investable.

But scale only compounds when the firm has architecture. If the data is poorly organized, inconsistently labeled, politically filtered, or impossible to audit, AI does not fix the problem. It accelerates it.

2. Extreme focus creates a different kind of scale

AI does not only help the biggest platforms. It also helps the most focused firms.

A small manager with genuine domain expertise can build a powerful advantage if every deal reviewed, every operator relationship, every lender discussion, every portfolio issue, and every failed thesis sits inside one narrow market.

This is a different kind of advantage. Not platform scale, but pattern recognition built over thousands of decisions.

A vertically focused manager does not need to know everything about private markets. It needs to know one market better than the generalist. It needs to know where the bodies are buried, which operating metrics matter, which sponsors overpay, which local markets are oversupplied, which lenders are pulling back, and which assumptions always look reasonable until they are stressed.

AI rewards that discipline because it can help organize a focused body of knowledge into a repeatable decision system.

The best small managers will not win by pretending to be smaller versions of mega-funds. They will win by being aggressively narrow.

The future isn't big versus small. The firms that win will have scale, focus, or a better way to make decisions.

3. The lower-middle-market M&A advisor is the stockbroker of this cycle

I learned this early in my career around lower-middle-market sell-side M&A.

There was real value in the work. A founder did not know every credible buyer. A buyer did not know every founder. The market was fragmented. The process was emotional. A good advisor could translate the story, create competitive tension, manage timing, pressure-test buyer credibility, and keep a fragile transaction from falling apart.

That skill still matters. But there was also a lot of brokerage economics hiding inside advisory language.

I remember how much of the process depended on friction: building the buyer list, packaging the company, drafting outreach, managing the data room, answering the same diligence questions, and convincing both sides that the process was more proprietary than it really was.

Some lower-middle-market M&A advisors are the stockbrokers of this cycle.

The old stockbroker benefited from information asymmetry and transaction costs. The client did not have the same information. The trade was expensive. Access had value. Then information became available, transaction costs collapsed, and the role had to evolve.

The same pressure is coming to parts of lower-middle-market M&A.

If AI can identify likely buyers, map acquisition criteria, summarize sector activity, compare precedent deals, draft outreach, screen add-on logic, generate diligence questions, and analyze buyer behavior, then "we know the buyers" is no longer enough.

The advisor who survives will not be the advisor with a list.

It will be the advisor who understands owner psychology, transaction risk, capital structure, buyer motivation, closing certainty, and the two or three issues that determine whether the deal actually gets done.

That distinction matters across the entire private markets value chain. Generic access is going down in value. Judgment-rich architecture is going up.

4. Headcount is no longer the moat

For years, resources were an easy advantage.

More analysts meant more screens. More associates meant more models. More consultants meant more slides. More databases meant more coverage. More junior people meant more hours.

That advantage is eroding.

My working assumption is blunt: one exceptional research analyst, paired with the right AI architecture, can produce 100 times the mechanical output of a traditional junior analyst in certain workflows.

That does not mean one person has 100 times the judgment. It means the scarce work is moving.

First-pass document review, model cleanup, transcript synthesis, comp screening, sponsor-background research, market mapping, diligence question drafting, and portfolio-monitoring summaries are all becoming cheaper.

The premium shifts to the person who knows what to ask. It shifts to the person who knows which output is wrong. It shifts to the person who can design the system, govern the data, define the underwriting standard, and decide when the answer is not good enough.

This is why the old analyst model is changing.

The analyst used to be paid to do the work.

The financial architect will be paid to design the system that decides what work matters.

5. Opacity will be solved by AI, but judgment will not be outsourced

Private markets have always been opaque. That opacity is part of the return opportunity. But opacity has also protected weak process, vague fees, stale marks, sponsor-friendly assumptions, and avoidable diligence gaps.

AI will not remove every information gap.

It will compress the cost of seeing through many of them.

Sponsor materials can be normalized. Models can be rebuilt. Assumptions can be compared. Reporting can be tracked against the original thesis. Market data can be layered in. Expert insight can be summarized. Negative signals can be escalated faster.

That is a major change.

But the architecture behind the process will still be human-driven. Someone has to decide which sources are trusted. Someone has to define the risk taxonomy. Someone has to decide whether a sponsor assumption is accepted, adjusted, challenged, or unsupported. Someone has to know when a model output is technically coherent but economically naive. Someone has to decide whether the investment deserves capital, attention, and monitoring burden.

That is the human job: not crunching the numbers, but making better decisions.

6. Investment services and financial research are at the edge of the change

Investment services and financial research are built on three activities: information gathering, synthesis, and judgment.

AI attacks the first two directly.

That does not make the third less valuable. It makes the third more visible.

A research provider that summarizes public information will be squeezed. A consultant that produces broad market commentary without decision utility will be squeezed. A placement process built around distribution will be squeezed. A generic diligence memo will be squeezed.

The market will not reward more paper. It will reward better systems.

The valuable output is not the memo itself. It is the process behind the memo: what was tested, what was challenged, what changed the conclusion, and what must be monitored.

The Scale or Focus Test

Allocators need a simple way to underwrite this future.

A private markets manager should be able to prove at least one of two things:

Scale: The firm has proprietary data, repeatable process history, portfolio intelligence, operating feedback loops, and enough institutional memory to make future decisions better.

Focus: The firm has a narrow domain where its expertise, network, pattern recognition, and diligence process are meaningfully better than a generalist's.

If the manager has neither, the allocator should assume the edge is decaying

The wrong question is: "Are you using AI?" The better question is: "What does your process know that the market does not?"

Where EM Capital fits

This is the work we are building around at EM Capital.

The allocator problem is not a lack of information. It is too much information arriving in forms that are difficult to compare, difficult to verify, and difficult to convert into a decision.

Sponsor decks. PPMs. Models. Track records. Reference calls. Reporting packages. Side letters. Market data. Fee schedules. Capital stacks. Liquidity terms.

Every opportunity arrives with its own vocabulary.

Allocators do not need more noise. They need a documented view.

EM Capital sits between raw sponsor materials and the allocator's decision forum. The objective is to convert sponsor materials into underwriting, monitoring, market intelligence, and decision-ready work product without acting as a product distributor or placement agent. The capabilities deck states that EM Capital does not receive sponsor placement fees, referral fees, transaction fees, or success fees, and that pipeline development is screening and research support, not capital raising.

That distinction is central.

We are not trying to replace allocator judgment. We are trying to expand allocator capacity.

Our process is built around normalization, independent analysis, risk escalation, and a documented view. Sponsor assumptions are not simply copied into a memo. They are accepted, adjusted, challenged, or marked unsupported, with rationale on the record.

That is the architecture.

It is also how we think about pipeline development and market intelligence. The best opportunities are not always the loudest inbound decks. Many of the most interesting managers are focused, specialized, and harder to evaluate without context.

Through pipeline development and market intelligence, we help allocators widen the aperture beyond inbound sponsor flow, filter opportunities by mandate fit, market signal, sponsor quality, and pricing window, and return a diligence read rather than a sales pitch.

Resi-Alpha is one example of the model.

It is not "AI makes the decision." It is an internal residential market intelligence platform that screens 386 U.S. metros for growth potential, overheating, bubble risk, and market stress using 300-plus inputs and analyst overlay. The key principle is governance: underwriting decides; the model informs.

That is the future of private markets research in one sentence.

The model informs. The architecture governs. The human decides.

What this means for allocators

Allocators should assume that every manager will soon sound more sophisticated.

Decks will be cleaner. Memos will be sharper. Market maps will be broader. Diligence packages will look more complete. AI will make mediocre materials look institutional.

That creates a new problem.

The allocator's job becomes separating polished narrative from durable edge.

The next diligence conversation should include harder questions:

What proprietary data informs your underwriting?

What have you learned from deals you passed on?

Where does your process reject opportunities faster?

Which assumptions are systematically challenged?

What part of your edge comes from scale?

What part comes from focus?

What remains human by design?

Private markets are not becoming less interesting. They are becoming more demanding.

This is an exciting time to be in private markets because the old excuses are getting weaker. Opacity will no longer protect lazy analysis. Headcount will no longer be enough. Distribution will no longer pass for insight. Generic research will no longer clear the bar.

The next generation of private markets advantage will belong to the firms that know exactly what they are.

Scaled platforms with proprietary memory.

Focused specialists with dense pattern recognition.

Allocators and advisors with real decision architecture.

Everyone else will be forced to explain what they actually do.

The next edge in private markets will not belong to the firms with the most analysts. It will belong to the firms with the best architecture.

Start with one. If you are reviewing a private markets manager whose edge depends on proprietary sourcing, deep specialization, or AI-enabled diligence, send us the package. We will return an independent one-page Decision Snapshot with no fee and no placement-agent relationship.